13.PNG

Caption

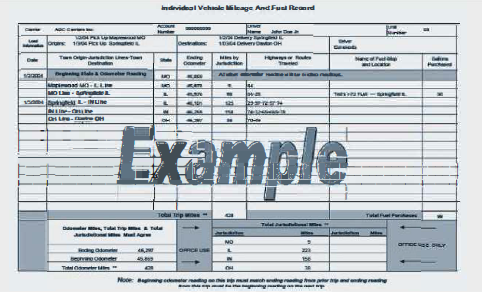

Figure 1.3: Individual Vehicle Mileage and Fuel Record (Example) An official website of the State of Georgia.

The .gov means it’s official.

Local, state, and federal government websites often end in .gov. State of Georgia government websites and email systems use “georgia.gov” or “ga.gov” at the end of the address. Before sharing sensitive or personal information, make sure you’re on an official state website.

Still not sure?

Call 1-800-GEORGIA to verify that a website is an official website of the State of Georgia.

If you operate a CDL required vehicle in interstate commerce, the vehicle, with few exceptions, is required to be registered under the International Registration Plan (IRP) and the International Fuel Tax Agreement (IFTA). These federally mandated programs provide for the equitable collection and distribution of vehicle license fees and motor fuels taxes for vehicles traveling throughout the 48 contiguous United States and 10 Canadian provinces.

Under the IRP, jurisdictions must register apportioned vehicles which includes issuing license plates and cab cards or proper credentials, calculate, collect and distribute IRP fees, audit carriers for accuracy of reported distance and fees and enforce IRP requirements.

Registrant responsibilities under the Plan include applying for IRP registration with base jurisdiction, providing proper documentation for registration, paying appropriate IRP registration fees, properly displaying registration credentials, maintaining accurate distance records, and making records available for jurisdiction review.

The basic concept behind IFTA is to allow a licensee (motor carrier) to license in a base jurisdiction for the reporting and payment of motor fuel use taxes.

Under the IFTA, a licensee is issued one set of credentials which will authorize operations through all IFTA member jurisdictions. The fuel use taxes collected pursuant to the IFTA are calculated based on the number of miles (kilometers) traveled and the number of gallons (liters) consumed in the member jurisdictions. The licensee files one quarterly tax return with the base jurisdiction by which the licensee will report all operations through all IFTA member jurisdictions.

It is the base jurisdiction's responsibility to remit the taxes collected to other member jurisdictions and to represent the other member jurisdictions in the tax collection process, including the performance of audits.

An IFTA licensee must retain records to support the information reported on the IFTA quarterly tax return.

The IRP registrant and the IFTA licensee may be the vehicle owner or the vehicle operator.

The requirement for acquiring IRP plates for a vehicle and IFTA license for a motor carrier is determined by the definitions from the IRP Plan and the IFTA for Qualified Vehicle and Qualified Motor Vehicle. For purposes of IRP:

If the vehicle you operate is registered under IRP and you are a motor carrier licensed under IFTA, then you are required to comply with the mandatory record keeping requirements for operating the vehicle. A universally accepted method of capturing this information is through the completion of an Individual Vehicle Distance Record (IVDR), sometimes times referred to as a Driver Trip Report. This document reflects the distance traveled and fuel purchased for a vehicle that operates interstate under apportioned (IRP) registration and IFTA fuel tax credentials.

Although the actual format of the IVOR may vary, the information that is required for proper record keeping does not.

In order to satisfy the requirements for Individual Vehicle Distance Records, these documents must include the following information:

An example of an IVDR that must be completed in its entirety for each trip can be found in Figure 1.3. Each individual IVDR should be filled out for only one vehicle. The rules to follow when trying to determine how and when to log an odometer reading are the following:

Not only do the trips need to be logged, but the fuel purchases need to be documented as well. You must obtain a receipt for all fueling and include it with your completed IVDR.

Make sure that any trips that you enter are always filled out in descending order and that your trips include all state and / or provinces that you traveled through on your route.

There are different routes that a driver may take, and most of the miles may be within one state or province. Whether or not the distance you travel is primarily in one jurisdiction or spread among several jurisdictions, all information for the trip must be recorded. This includes the dates, the routes, odometer readings and fuel purchases. By completing this document in full and keeping all records required by both the IRP and the IFTA, you will have ensured that you and your company are in compliance with all State and Provincial laws surrounding fuel and distance record keeping requirements.

The IVDR serves as the source document for the calculation of fees and taxes that are payable to the jurisdictions in which the vehicle is operated, so these original records must be maintained for a minimum of four years.

In addition, these records are subject to audit by the taxing jurisdictions. Failure to maintain complete and accurate records could result in fines, penalties and suspension or revocation of IRP registrations and IFTA licenses.

For additional information on the IRP and the requirements related to the IRP, contact your base jurisdiction motor vehicle department or IRP, Inc. the official repository for the IRP. Additional information can be found on the IRP, Inc. website at www.irponline.org. There is a training video on the website home page available in English, Spanish and French.

For additional information on IFTA and the requirements related to IFTA, contact the appropriate agency in your base jurisdiction. You will also find useful information about the Agreement at the official repository of IFTA.